Salesforce: Grandpa's still got it

Here's a question: what companies have had the most reliable track record of revenue growth over the past 15 years? Who would you guess?

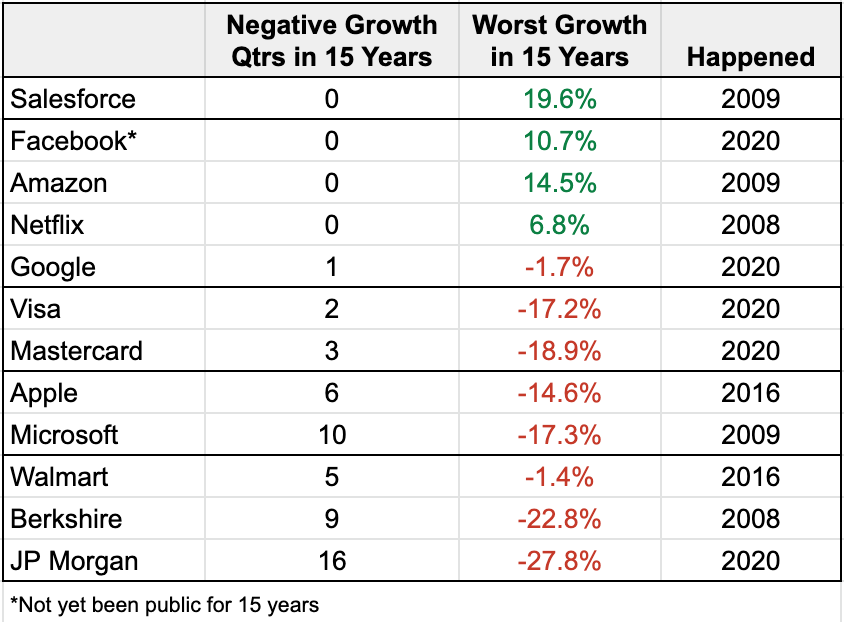

You might think: historical giants like Walmart, Berkshire Hathaway, or JP Morgan. But you'd be wrong - among them they've had 30 negative growth quarters in the last 15 years.

You might think: tech institutions like Microsoft or Apple. Again, you'd be wrong. They've had 16 negative growth quarters.

You might think: the Visa / Mastercard credit card duopoly. You'd be getting a bit closer but even they could not withstand the pandemic, registering their first 5 negative growth quarters last year.

What about the FANG companies? Spot on. Incredibly, just one negative quarter between all four of them in 15 years. One!

It might never occur to you to think of Salesforce. But not only have they grown every quarter for 15 years straight, the slowest growth was better than any company we've mentioned.

This has led to revenue growth so predictable, the graph looks like it was made up:

This predictability allows the company to project the future like no other company does. At a time when many have withdrawn financial guidance, Salesforce is telling us where they'll be in FIVE years:

If all this is true then why is Salesforce still often overlooked? Here are some of the most common criticisms I've read:

Nobody likes the product. Won't their customers churn?

They've been at it for 20 years. How much growth is left?

They paid way too much for Slack. What does that have to do with CRM?

Enterprise software is really boring. I could be trading $GME right now

Let's dig into each one:

💀 Nobody likes the product. Won't their customers churn?

Actually, that almost happened in 2005. Salesforce had a near-death experience from churning almost 100% of its customers. But they managed to pivot the entire company to tackle this problem:

...a man named David Dempsey did at a corporate retreat in the spring of 2005 was nothing short of heroic. Previously, Dempsey, an Irishman, had run a team expanding Salesforce's European footprint.

At the time of this fateful meeting, he'd been tasked with the responsibility of managing customer renewals. His presentation to the executive team left little room for interpretation.

Salesforce needed to fix this customer churn problem or else. Dempsey did such a masterful job of painting a disastrous "or else" that he became known throughout the C-suite as Dr. Doom.

These are the experiences that make their way into the DNA of a company. Today Salesforce’s retention is best-in-class among enterprise software companies (source) and I don't expect the lessons from 2005 to be forgotten.

To be fair, I still don't hear much fanfare about the product itself. It is very much still an enterprise solution in the classic sense: expensive, complex to configure, and requires specialized skills to maintain. But over the years, these characteristics have given birth to a massive ecosystem built around Salesforce.

Some of the most interesting stats:

The ecosystem will make about $100B in 2021 (over four times what Salesforce makes directly)

The ecosystem will create 3.3M high paying jobs by 2022 (over fifty times the number employed by Salesforce directly)

The Dreamforce conference drew 170k attendees in 2019 (bigger than Microsoft, Amazon, and Google's cloud conferences combined)

The sheer size of this ecosystem has become a wide moat vs competitors and powerful insulation from churn.

🕰 They've been at it for 20 years. How much growth is left?

Salesforce is best known for its namesake - the cloud CRM product to manage your sales team. But it might surprise you to learn that sales CRM now accounts for just 24% of the company's revenue. In fact, it isn't even the largest product offering anymore. Over the years, Salesforce has expanded into adjacencies using some of the best M&A game in town. Their largest acquisitions have also appreciated substantially in value:

Note: I believe these estimated valuations are conservative. Not only are they based on 2019 revenue but the multiples used are lower than equivalent industry benchmarks.

With each one, Salesforce integrated the foundation for a whole new product cloud they could upsell their existing customers on. And get ready for more because Salesforce is the only company in the world that can make the following pitch to founders of promising targets:

Cash in your chips and keep running your company

Check out our track record. Every major acquisition has benefited from our distribution power

Avoid the slow descent to irrelevance (vs acquisition by IBM, ORCL or SAP)

Avoid the bright lights of antitrust (vs acquisition by MSFT, GOOG or AMZN)

This playbook has allowed Salesforce to expand its TAM from $30B in 2013 to an estimated $176B in 2024 (21% CAGR).

A quick aside: Salesforce's venture game ain't bad either. They've invested hundreds of millions in nCino, Snowflake, and Zoom over the last two years. Those investments are already up 2-3x.

💬 They paid way too much for Slack. What does that have to do with CRM?

In December, Salesforce announced it is acquiring Slack for $27.7B. Let's just say Wall Street was not thrilled about it:

It’s worth noting that investors are not showing signs, initially at least, of liking this deal, with the stock down over 8% today and 16.5% since the rumor of Salesforce’s interest in Slack surfaced last week before the Thanksgiving holiday. That translates into more than $18 billion in lost market cap...

But consider this: what if the acquisition isn't just about adding team communications to the Salesforce product suite? What if it is just as impactful at leveling up the rest of Salesforce?

Remember how nobody likes Salesforce's product? Guess who has built one of the most engaging products ever?

Remember how Salesforce is a classic enterprise sales company? Guess who has been a case study in product-led growth?

And finally, keep in mind that Salesforce's M&A track record is pretty good. At the very least, I think we can expect their massive ecosystem to provide a boost to Slack's already-fast growth. As a result, while Wall Street may not be excited, SaaS executives and venture investors have been a lot more optimistic:

We probably won't know for another year or two whether this was a smart move. But for new investors in Salesforce, you get to take this bet at a nice discount from the November price.

😴 Enterprise software is really boring. I could be trading $GME right now

Fine, that one is true. Salesforce is not going to rocket up 100% a day. But in a zero interest rate world and record market caps all over, boring can be good. Boring can lead to good long term value.

It currently trades at an Enterprise Value around $200B which is...

Within 10% of its 3-year EV/NTM revenue median (even though the SaaS industry has become twice as expensive by that metric)

Just 4x FY2026 revenue guidance (Oracle is more expensive than that with zero growth in the last three years)

Priced near the industry's "low-growth" benchmark even though Salesforce would be classified as a "mid-growth" company with its 19% consensus NTM revenue growth (source)

I’m more than happy to own Salesforce and completely forget about it until it publishes its plan to get to $100B in revenue.

Next Thesis is long Salesforce with an average cost basis of $221.70 as of publishing. Assume the usual disclaimers. This is not investment advice. Do your own research before investing.